On 12 June 2026, the US Division of Commerce issued an emergency directive that compelled Anthropic to droop overseas nationals from utilizing Claude Fable 5. It got here all of the sudden with no exemption for allied nations and no appeals course of. One jurisdiction flipped a swap, and the world’s entry to a number one piece of frontier synthetic intelligence (AI) went darkish.

The ban, which the US has solely now begun to raise after weeks of diplomatic fallout, marks greater than an AI security controversy. It crystallises a query that European and UK policymakers have been racing to reply by an unprecedented wave of legislative and industrial interventions. Specifically, when a single nation controls the infrastructure upon which your financial system, public companies and nationwide safety rely, what does sovereignty truly imply – and might you construct it shortly sufficient?

This text examines whether or not Europe and the UK can shut a digital sovereignty hole that many years of dependence on American expertise have rooted within the continent’s financial foundations. Drawing on financial information, historic precedent and educational evaluation, it appears at whether or not catch-up stays attainable and checks that in opposition to three stipulations demonstrated by profitable late-developer states in trendy historical past. These are unified strategic funding at a scale that matches the competitors, the willingness to make use of inside markets as an exclusionary weapon, and the humility to repeat relatively than insist on innovating.

Urgency in Brussels and Westminster

The latest flurry of coverage bulletins means that Brussels and Westminster are gripped by some urgency.

The European Union’s (EU) Cloud and AI Growth Act – a part of the European Fee’s AI Continent Motion Plan – proposes a single EU-wide sovereignty framework with 4 escalating ranges of autonomy, from primary bodily information residency (Degree 1) by to full software program provide chain transparency and demonstrated independence from third-country interference (Degree 4). The act additionally targets a threefold enlargement of European datacentre capability by the 2030s, backed by streamlined allowing and improved entry to vitality, land and financing.

Alongside this sits the Chips Act 2.0, which shifts the EU’s semiconductor technique from supply-focused funding to demand cultivation. Its predecessor mobilised greater than €52bn in private and non-private funding and created an estimated 46,000 jobs. The sequel introduces “grand challenges” geared toward industrial improvement of AI-critical chips, demand accelerators to hurry merchandise to market, and state support provisions for first-of-a-kind fabrication initiatives not but current within the Union.

The EU Open Supply Technique completes the triad, mandating public administrations to behave as anchor customers of open supply alternate options – cloud, office instruments, safe electronic mail – and creating a sovereign “Open Web Stack” designed to displace proprietary overseas software program from authorities workflows.

The UK, working outdoors EU mechanisms however going through an identical structural vulnerabilities, has assembled its personal arsenal. The £1.1bn sovereign compute technique – introduced by expertise minister Liz Kendall with the declaration that “AI is the defining forex of financial and onerous energy in at the moment’s world” – allocates £750m to a nationwide AI supercomputer, together with £400m for specialist chip procurement. A £120m AI {hardware} innovation programme funds home chip design and testing. The £500m Sovereign AI Unit, launched in April 2026, goals to turn out to be the first funding hub for high-potential UK AI startups, whereas a separate £500m sovereign AI fund targets growth-stage firms with investments between £1m and £10m.

The important thing levers of digital sovereignty

These measures could be grouped into 4 strategic levers that the EU and UK are pulling concurrently:

Provide-side industrial coverage – the state instantly funding bodily infrastructure to bypass market reliance on overseas hyperscalers.

Procurement-led sovereignty – utilizing public sector buying energy to set market requirements and drive technical necessities on suppliers, from open supply mandates to native information residency.

Regulatory shielding – establishing authorized frameworks, reminiscent of France’s SecNumCloud 3.2 qualification and Germany’s BSI C3A two-tier cloud autonomy standards, that drive overseas suppliers to satisfy sovereignty definitions or face exclusion from authorities workloads.

Innovation ecosystem assist – focused grants and funding funds designed to domesticate homegrown mental property.

The cumulative funding is substantial on paper. But it surely should be measured in opposition to a worldwide expertise financial system by which the imbalance of energy will not be solely giant however structural.

Information reveals US digital dominance

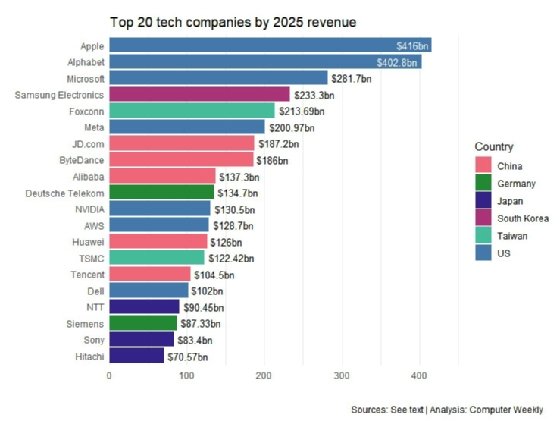

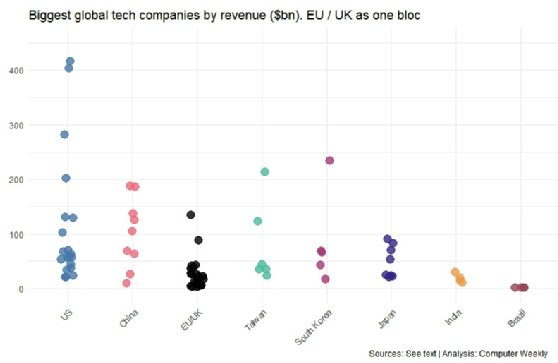

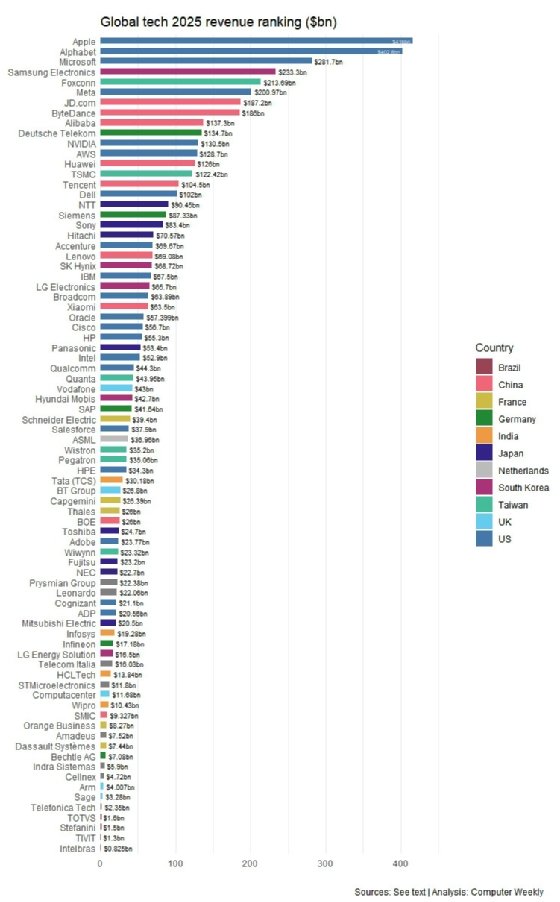

Pc Weekly evaluation of audited annual experiences and regulatory filings, benchmarked in opposition to World Financial institution and IMF GDP statistics, reveals that US-headquartered expertise corporations generated mixed international revenues exceeding $2tn of their most up-to-date fiscal years.

Microsoft alone posted $281.7bn – greater than the mixed tech income of each main agency headquartered in France, Italy, Spain and the UK, and rivalling Germany’s whole listed tech sector.

Amazon Net Providers (AWS) contributed $128.7bn in cloud infrastructure income, Alphabet $402.8bn, and Nvidia – the semiconductor designer whose graphics processing models (GPUs) energy the AI revolution – $130.5bn.

In contrast, Europe’s largest expertise firms function at a fraction of that scale. Germany’s SAP, the continent’s flagship enterprise software program agency, reported $41.6bn. France’s Dassault Systèmes reached $7.4bn. The UK’s ARM – a globally important semiconductor mental property (IP) designer – generated $4bn.

No European-headquartered firm operates a hyperscale cloud infrastructure enterprise at a stage aggressive with AWS, Microsoft Azure or Google Cloud. The supply mannequin that underpins the trendy digital financial system – elastic, on-demand compute – is nearly solely American-owned.

Tech GDP as a share of nationwide output tells the identical story from a distinct angle.

The US tech sector accounts for 7.1% of GDP in opposition to a $30.5tn financial system. The UK sits at 5%, Germany at 5.1%, France at 5.2%. The hole seems modest till measured in opposition to the international locations which have already caught up. South Korea registers 12.3% tech GDP – the very best of any superior financial system – constructed on Samsung Electronics ($233.3bn), SK Hynix ($68.7bn), and a state equipment that for many years directed credit score to particular corporations by state-directed credit score mechanisms. Taiwan hits 12% on the again of TSMC ($122.4bn) and Foxconn ($213.7bn), firms incubated beneath circumstances of strategic state safety and express authorities coordination.

The state as driver of improvement

What distinguishes the South Korean and Taiwanese outcomes from European aspirations will not be merely the size of funding however the political structure that directed it.

Andrew Wright, a lecturer at Hult Worldwide Enterprise Faculty who specialises in worldwide political financial system, frames the excellence by the lens of historic catch-up dynamics.

“Germany and America overtook British management by protectionism and state promotion of business,” notes Wright. “In consequence, they developed large monopolistic – or, extra precisely, oligopolistic – company giants. Scale was vital then and nonetheless is.”

The post-war era of East Asian builders – Japan, then Korea, then Taiwan – intensified this mannequin.

“These international locations used rather more in depth state assist, safety, and, frankly, general route,” Wright explains. “All of those states borrowed and stole expertise, promoted large corporations, protected house markets and largely copied superior nations whereas benefiting from decrease prices.”

The sample is so constant that the financial historian Alexander Gerschenkron recognized a typology: the later the catch-up venture, the higher the function performed by the state. China, the latest entrant, represents the apotheosis of this trajectory – state capitalism at continental scale, with Alibaba ($137.3bn), Tencent ($104.5bn) and Huawei ($126bn) now rivalling Western incumbents on income and more and more on technological functionality.

However the East Asian precedent carries a complicating factor for Europe.

Low cost labour – the mechanism that enabled Korea and Taiwan to drive export-led progress whereas defending home markets – is structurally unavailable to superior European economies.

“Europe can not emulate this in competing with the US,” Wright argues. The extra related parallel lies additional again in historical past. “Within the late nineteenth century, low wages weren’t a significant factor within the rise of the US and Germany. It was extra about state tutelage, the expansion of the large company, and the systematisation of analysis and improvement.”

Responding at scale hampered by fragmentation

This distinction proves crucial when evaluating the three stipulations in opposition to Europe’s current place.

The primary prerequisite – unified strategic funding at a scale that matches American finance – faces the quick impediment of fragmentation. The UK’s £1.1bn sovereign compute programme and the EU’s €52bn Chips Act mobilisation signify real political dedication, however they function by solely separate governance buildings, procurement pipelines and strategic priorities.

South Korea’s window steerage system, by which the central financial institution actually directed non-public banks to increase credit score to designated corporations, required a focus of economic authority that no European establishment – not the European Funding Financial institution, not the European Central Financial institution, not any nationwide treasury – at present possesses.

“Solely a massively concentrated strategic mechanism of funding can compete with what the Individuals now have accessible to them,” Wright observes, “partly as a result of their previous and partly as a result of sheer dimension of American finance.” He provides: “Present efforts to seed little developmental pockets, or the shoots of enterprise capitalism, can not probably compete.”

Utilizing the market: The Airbus instance

The second prerequisite – the willingness to make use of Europe’s inside market as an exclusionary weapon – has a confirmed precedent.

Airbus, the European aerospace consortium, now competes instantly with Boeing after many years of state-backed improvement that American free-market economists as soon as derided as incapable of selecting winners.

I’d see Airbus as a mannequin. If I used to be a pro-EU coverage maker, I’d cease American non-public firms from feeding off funds and contracts of the European states, and change these relations with European contractors Andrew Wright, Hult Worldwide Enterprise Faculty

“I’d see Airbus as a mannequin,” says Wright. The logic transfers on to digital infrastructure: “If I used to be a pro-EU coverage maker, I’d cease American non-public firms from feeding off funds and contracts of the European states, and change these relations with European contractors.”

Components of this method are already seen. The UK’s Science, Innovation and Know-how Committee has proposed a “cloud consumption dashboard” to publicly observe contract awards by provider, mandating SME spending targets and break clauses in contracts with overseas suppliers. The Procurement Act 2023 is being up to date to require public sector our bodies to prioritise open supply options. The EU’s four-level sovereignty framework creates a ratcheting mechanism by which suppliers should reveal progressively deeper independence from third-country jurisdiction to qualify for delicate workloads.

The counter-current, nevertheless, is highly effective. A long time of procurement choices have entrenched American hyperscalers inside European public sector structure.

The community results are self-reinforcing. The extra departments standardise on a single cloud platform, the tougher and costlier exiting turns into.

Wright describes this as “path dependence” – the accrued weight of previous decisions that makes deviation pricey even when the strategic case for change is overwhelming. “Europe has existed beneath American tutelage, permitting US corporations entry and the event of dominance,” he notes. “Breaking out of that is pricey and troublesome.”

Copy, don’t innovate

The third prerequisite – the willingness to repeat relatively than insist on innovating – cuts in opposition to Europe’s self-conception as a centre of unique analysis.

Wright factors to a historic irony. “A lot of the expertise that has fed the American machine was initially developed in Europe. But Europe has usually been unable to manage and commodify it, or construct the large dominant corporations that emerged from it,” he says.

The East Asian builders confronted no such cultural constraint. “They hardly ever innovated; they largely copied,” says Wright.

The EU Open Supply Technique represents an implicit acknowledgement of this logic – constructing a listing of open alternate options that, by definition, replicate proprietary performance relatively than inventing from scratch. The Gaia-X federated infrastructure initiative creates interoperability requirements designed to let native European suppliers hyperlink companies in direct competitors with non-EU hyperscalers, once more a copying-and-competing mannequin relatively than a leapfrogging one.

Whether or not European political tradition can maintain this pragmatic posture – constructing what works relatively than what’s unique – stays an open query.

Digital sovereignty at a crossroads

The query that faces European policymakers will not be whether or not digital sovereignty is fascinating however whether or not the window for reaching it stays open.

The Fable 5 episode demonstrates that dependency will not be a theoretical threat that may be managed by contractual high quality print. It’s an operational actuality that may be triggered by a overseas authorities’s unilateral determination, with penalties that cascade by each service, each division, and each citizen who depends on infrastructure they don’t management.

The income information suggests the structural hole is widening, not closing. American expertise corporations develop at charges European rivals can not match, fuelled by a enterprise capital ecosystem, a inventory market depth and a military-industrial procurement pipeline that Europe has no equal of.

The US, Wright argues, operates a “hidden developmental state” – much less visibly directive than the East Asian mannequin however no much less efficient, leveraging defence spending, public sector contracts and deep state-corporate integration to maintain technological dominance whereas sustaining the rhetorical posture of free enterprise.

The conditional verdict, then, is that Europe and the UK can catch up – however the path calls for a stage of political coordination, monetary focus and strategic pragmatism that the continent has hardly ever mustered outdoors of wartime mobilisation or the Airbus venture.

The measures now being deployed are real in intent and substantial in scale by historic European requirements. Whether or not they’re adequate in velocity and coordination to beat many years of accrued dependency is the query on which the subsequent decade of European digital sovereignty will flip.