Hyperscaler datacentres set to dominate by 2031

Immense focus continues apace within the cloud business, with hyperscalers anticipated to comprise 67% of world datacentre capability by 2031, or 14 instances the capability they’d in 2018. Again then, enterprise datacentres accounted for 56% of all datacentre capability.

That’s in response to figures from US-headquartered analysis organisation Synergy Analysis Group, which says synthetic intelligence (AI) is driving big and accelerated progress, with hyperscaler capability anticipated to double within the subsequent three years.

By the fourth quarter of 2025, Synergy discovered that hyperscaler-operated datacentres accounted for 1,360 of whole websites and 48% of worldwide capability. Datacentres constructed by hyperscalers kind the majority of that capability – 60% of it – with the remaining capability leased.

Non-hyperscale colocation capability accounts for 20% of present totals, whereas enterprise datacentres account for 32%.

Synergy expects hyperscaler datacentre capability to comprise 67% of all capability in 2031. The share of colocation is anticipated to drop, though it’s nonetheless growing at double-digit charges.

Enterprises’ on-premise datacentre capability is anticipated to drop to 19% of the whole by 2031, at a charge of about 2% per yr, though even right here that decline just isn’t so fast, largely as a result of deployment of AI {hardware}.

Synergy’s information relies on a number of quarterly monitoring analysis providers in hyperscale, colocation and enterprise datacentres, and primarily based on datacentre footprint and operations of the world’s main cloud colocation corporations, plus monitoring the datacentre {hardware} market.

John Dinsdale, a chief analyst at Synergy Analysis Group, mentioned AI is driving the world’s datacentre market in the direction of elevated focus in favour of the hyperscalers.

“Cloud and consumer-oriented digital providers have been driving adjustments in datacentre deployment patterns for a few years now, however over the past three years, AI expertise has accelerated these adjustments,” he mentioned.

“We’re seeing a special mixture of datacentre utilization throughout the areas, however total, the world is racing in the direction of a state of affairs the place hyperscale operators are liable for the majority of world datacentre capability. There are virtually 800 hyperscale datacentres in our identified future pipeline, enabling hyperscale capability to double in simply three years,” Dinsdale added.

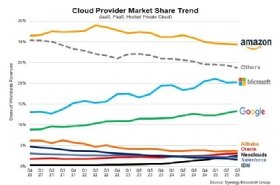

By the third quarter of 2025, worldwide spend on cloud providers had reached $107bn, up from $68bn two years earlier than that, in 2023.

Among the many massive three, Amazon’s market share has been in a state of gradual decline since 2022. Within the third quarter of 2025, it had a 29% market share, down from just below 34% within the third quarter of 2022.

In the meantime, the third-quarter 2025 market share for Microsoft was 20%, and 13% for Google Cloud. Each of those are seeing will increase in market share, with Microsoft up from 13% within the fourth quarter of 2020.

In the meantime, so-called neocloud suppliers – people who specialize in AI datacentre capability – have a market share of two.5%.

Dinsdale mentioned: “Past the three market giants, a large mixture of smaller gamers is competing for traction, however the actuality is that third-placed Google stays almost 4 instances the scale of fourth-placed Alibaba, underscoring the widening gulf between the market leaders and the remainder of the sector.”