Information dive: A brand new American Century within the datacentre pipeline?

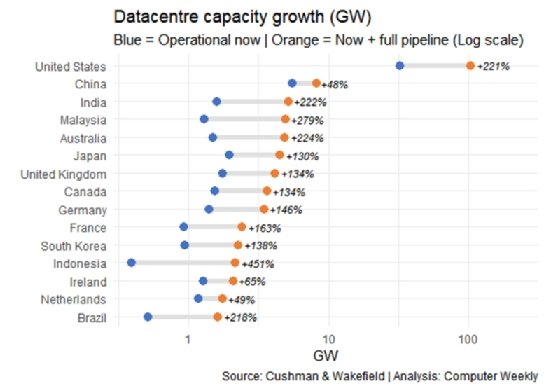

It appears to be like like we’re heading for a brand new American Century with regards to datacentre improvement, with US capability set to triple to a staggering 102GW if all projected capability within the pipeline involves fruition.

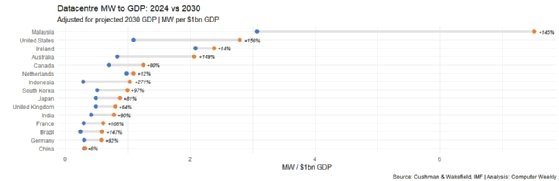

In the meantime, the UK – with about 1.7GW at present – will attain about 4GW, and appears set to slide within the rankings when it comes to absolute datacentre capability and when it comes to megawatts (MW) to gross home product (GDP).

That’s in line with figures from business property agent Cushman & Wakefield, plus GDP information from the Worldwide Financial Fund (IMF), with evaluation by Pc Weekly.

Additionally within the US, Virginia is ready to retain its nickname of “datacentre alley”, with capability within the pipeline that may see it retain its primary area rating and take it to greater than 10GW. London, nevertheless, may transfer up the rankings right here to change into the sixth largest datacentre area if all deliberate capability is constructed.

UK datacentre capability set to slide

The UK at present ranks fourth in megawatt capability phrases – behind the US, China and Japan – with about 1.76GW of capability. However it should slip to seventh when it comes to complete operational and deliberate capability, with India, Malaysia and Australia set to leapfrog it.

The UK ranks eighth at present when it comes to MW to GDP, however will slip to tenth if we measure all present and deliberate capability.

By way of datacentre regional capability, London ranks eighth with 1.53GW. It stays at eighth if tasks below development are taken under consideration (rising to 1.82GW), however jumps to sixth if the overall pipeline is taken into account (3.25GW), though that will embody tasks that haven’t gained planning consent and will by no means achieve this.

It’s potential that “London” takes under consideration far more than that area in Cushman & Wakefield’s figures, nevertheless. Pc Weekly analysis (see field: Nailing down datacentre pipeline numbers) into put in datacentre capability has the entire of the UK at about 1.6GW, together with the M62 area plus the North East and Scotland.

Eire at present lies tenth when it comes to put in capability, with 1.27GW. It slides to thirteenth when it comes to complete below development and pipeline, at round 2GW. However when it comes to MW to GDP, it sits second, solely dropping to 3rd after we measure at present put in and all pipeline in opposition to the projected 2030 GDP.

Indonesia and Malaysia set for big relative development

Whereas the US appears to be like decided to take care of its place on the earth datacentre rankings – it has a projected capability development charge of 221% – it’s outstripped in development phrases by some nations that look eager to develop datacentre capability.

The taking pictures star amongst these is Indonesia, with projected development of 451% in capability phrases (to 2.1GW). Behind it’s Malaysia at 279% projected development (to 4.87GW).

They seem like aiming at turning into suppliers of datacentre capability for regional economies similar to Singapore, Thailand and Vietnam.

Singapore had been the dominant regional hub, however energy and land constraints noticed it name a halt to additional datacentre improvement. This has been considerably reversed, however Indonesia and Malaysia have seen a chance to utilize their sources, with Amazon, Google, Microsoft and Meta pledging billions of {dollars} in direction of datacentre tasks there.

Information sovereignty a giant issue for some

In the meantime, the Cushman & Wakefield numbers present development in datacentre capability of 200% or extra for Australia, India and Brazil.

Australia advantages from huge quantities of land and renewable power, allied with a few of the world’s strictest information sovereignty legal guidelines. The latter has compelled big native builds that wouldn’t exist if the information might be hosted in cheaper regional hubs. It’s set for datacentre capability development of 224% (to 4.8MW) and MW to GDP development of 149%.

India’s sizeable development – 222% in capability (to five.1MW) and 90% development in MW to GDP – is pushed by regulatory mandates, a gargantuan home person base and structural price benefits. India has applied a few of the world’s most stringent information residency necessities. Additionally, world firms that beforehand served India from hubs in Singapore or Dubai are actually legally required to construct or lease bodily capability inside India.

Brazil advantages from being a key financial centre for South America, is a main touchdown level for subsea cables on the continent, has a lot of renewable power and – that is turning into a theme – has strict information sovereignty necessities. It has a projected capability development charge of 218% (to 1.6GW) with a MW to GDP development of 147%.

Right here, equally to India, Brazilian regulation encourages firms to retailer the information of Brazilian residents on-shore, which has compelled cloud suppliers to develop native areas in São Paulo and Rio de Janeiro.

In Europe, in the meantime, the UK, France and Germany are hitting structural limits when it comes to energy provide, with waits measured in years to get a grid connection. On the identical time, there’s a shortage of land and strict sustainability necessities.

Having mentioned that, these are mature markets, and the place there are constraints when it comes to new development in established centres, that’s now shifting in direction of different areas in close by nations similar to Italy, Spain and Poland, or inside nations, such because the shift north within the UK.

Maxed out Paddy

Eire, particularly Dublin, constructed out its capability years earlier than the remainder of Europe, however was the primary main world hub to hit a “grid ceiling”. Present capability is 1.2GW. Since 2021, state-owned grid operator EirGrid has applied a practical moratorium on new datacentre connections within the larger Dublin space. By 2024, datacentres consumed 21% of Eire’s complete electrical energy – greater than all its houses mixed.

Now, below new rules, if an organization needs to construct a brand new datacentre of greater than 10MW, they need to present their very own on-site technology – like gasoline generators or battery arrays – to again up 100% of their demand.

In the meantime, Eire is the European headquarters for nearly each main US tech agency, and since they e book earnings in Eire, GDP is roughly 40% larger than the precise worth produced by the Irish inhabitants. So, its MW to GDP development charge in these figures is 5.7%.

For that motive, Eire’s GDP is taken into account unreliable for measuring precise home financial well being.

What does MW to GDP inform us?

If we measure a rustic’s datacentre capability in megawatts (MW) in opposition to its gross home product (GDP), we get some thought of whether or not that capability is primarily a utility supporting its personal home economic system or successfully an export designed to course of information for the remainder of the world.

By taking a look at how that may change, we will additionally see the trajectory of that nation relative to its digital economic system.

The ratio of MW to GDP is a measure of digital infrastructure in comparison with the economic system extra broadly. Within the datacentre age, it’s like measuring “miles of observe per capita” or “metal manufacturing per GDP” as measures of business improvement.

We are able to see from the numbers that differing fashions emerge.

Very excessive ratios of MW capability to GDP – for instance, Eire, Indonesia, Malaysia – counsel a rustic positioned as a “digital exporter”. They eat energy domestically to course of information for different nations. Their MW capability is excessive, whereas GDP is low.

In the meantime, very low ratios of MW capability to GDP – for instance, Japan, the UK, the Netherlands – will typically be mature, service- or manufacturing-heavy economies the place datacentres assist home enterprise somewhat than act as an export.

Many of the world’s developed economies fall into the latter class, whereas some fast movers from a less-developed start line fall into the previous.

Two nations, nevertheless, appear set for fast however balanced development – the US and Australia. They’re each nations with huge house and scope for renewable power, and so they have developed economies. With projected MW to GDP development of 150% or extra, that might point out a candy spot when it comes to financial improvement.